There is a mortgage underwriting model in your roadmap that will approve and price loans faster and more accurately, and the team is focused on its predictive performance. What the plan has not centered is that underwriting is governed by fair lending law: the model must not discriminate on protected characteristics, even indirectly through proxies, its decisions must be explainable to applicants and regulators, and it must be tested for disparate impact. A more accurate model that cannot meet those requirements is not an advance; it is a fair lending violation waiting to be found.

This is more than a performance model. It is mortgage underwriting where fair lending compliance is a design requirement, not an add-on.

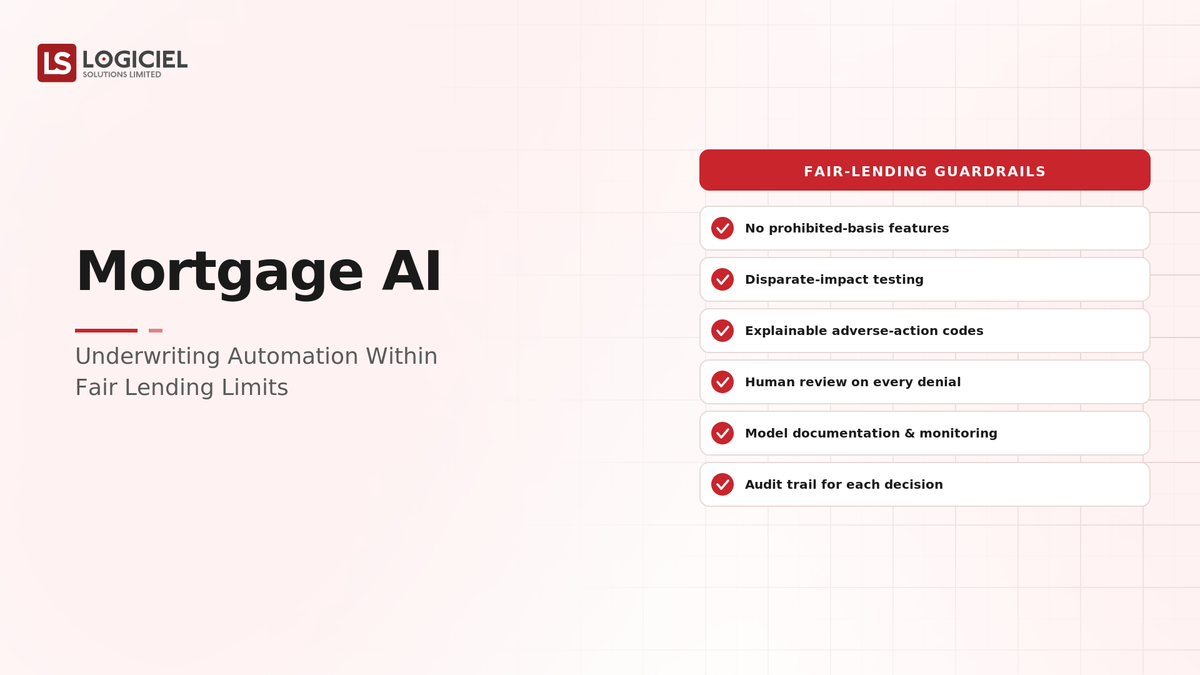

Mortgage AI within fair lending limits is more than an accurate underwriting model. It is a system designed so its decisions do not discriminate on protected characteristics, directly or through proxies, can be explained to applicants and regulators as the law requires, and are tested for disparate impact. Fair lending is not a compliance review at the end; it shapes the model's features, explainability, and testing from the start.

However, many teams optimize underwriting accuracy and confront fair lending late, when proxy features, unexplainable decisions, and untested disparate impact are already built in.

If you are a lending or technology leader building underwriting AI, the intent of this article is:

- Define what fair lending requires of an underwriting model

- Walk through explainability, proxy avoidance, and disparate-impact testing

- Lay out the controls a compliant model needs

To do that, let's start with the basics.

AI Products Fail Because of Infrastructure

They’re stuck because the data layer they need doesn’t exist yet

What Is Fair-Lending-Compliant Mortgage AI? The Basic Definition

At a high level, fair-lending-compliant mortgage AI is an underwriting system designed so its decisions do not discriminate on protected characteristics, directly or through proxies, are explainable to applicants and regulators, and are tested for disparate impact, with fair lending shaping the design rather than reviewed afterward.

To compare:

If an accurate-but-uncompliant model is a powerful engine that fails emissions, fair-lending-compliant mortgage AI is the same predictive power built to pass the legal standards underwriting must meet. Performance alone is not enough in a regulated decision; the model must be designed to be lawful and explainable.

Why Is Fair Lending Compliance Necessary?

Issues that fair lending compliance addresses or resolves:

- Ensuring underwriting does not discriminate, directly or by proxy

- Making decisions explainable to applicants and regulators

- Testing for and managing disparate impact

Resolved Issues by Compliant Design

- Avoids proxy discrimination on protected characteristics

- Produces explainable underwriting decisions

- Tests and manages disparate impact

Core Components of Compliant Mortgage AI

- Features avoiding protected characteristics and their proxies

- Explainability of underwriting decisions

- Disparate-impact testing

- Documentation for regulatory defensibility

- Governance of the model over time

Modern Mortgage AI Considerations

- Feature selection avoiding proxies

- Explainable model approaches

- Disparate-impact and fairness testing

- Adverse-action explanation requirements

- Ongoing fairness monitoring

These shape compliant underwriting AI; the discipline is designing for fair lending from the start, not reviewing afterward.

Other Core Issues They Will Solve

- Provide a defensible fair lending position

- Enable faster underwriting within legal limits

- Support required applicant explanations

Importance of Fair Lending Compliance in 2026

Designing for fair lending matters more as AI underwriting grows. Four reasons explain why it matters now.

1. Underwriting is legally governed.

Mortgage underwriting is governed by fair lending law. A model that discriminates, even by proxy, is a violation regardless of accuracy.

2. Proxies create indirect discrimination.

A model can discriminate indirectly through features correlated with protected characteristics. Avoiding proxies is essential, not optional.

3. Explainability is legally required.

Applicants are entitled to explanations for adverse decisions, and regulators expect them. An unexplainable model cannot meet this.

4. Disparate impact must be tested.

Fair lending requires testing for disparate impact. An untested model carries unknown, unmanaged risk.

Traditional vs. Compliant Mortgage AI

- Optimize accuracy alone vs. design for fair lending

- Any predictive feature vs. features avoiding proxies

- Opaque decisions vs. explainable decisions

- Compliance review at the end vs. fair lending designed in

In summary: Fair-lending-compliant mortgage AI avoids proxies, is explainable, and is tested for disparate impact, with fair lending shaping the design from the start.

Details About the Components of Compliant Mortgage AI: What Are You Designing?

Let's go through each element.

1. Feature Layer

What the model uses.

Feature decisions:

- Protected characteristics excluded

- Proxies for protected characteristics avoided

- Features vetted for indirect discrimination

2. Explainability Layer

Explaining decisions.

Explainability decisions:

- Decisions explainable to applicants and regulators

- Adverse-action reasons producible

- Transparency in the model's drivers

3. Disparate-Impact Layer

Testing for fairness.

Disparate-impact decisions:

- Testing for disparate impact across groups

- Impact measured and managed

- Risk identified before deployment

4. Documentation Layer

Defensibility.

Documentation decisions:

- Design and testing documented

- Feature legitimacy recorded

- A defensible regulatory record

5. Governance Layer

Ongoing compliance.

Governance decisions:

- Fairness monitored over time

- Drift in impact detected

- Ongoing fair lending governance

Benefits Gained from Compliant Design

- Underwriting that does not discriminate, directly or by proxy

- Explainable decisions meeting legal requirements

- Tested, managed disparate impact

How It All Works Together

The model is designed to exclude protected characteristics and to avoid features that act as proxies for them, with features vetted for indirect discrimination. Its decisions are explainable to applicants and regulators, so adverse-action reasons can be produced as the law requires. Before deployment and on an ongoing basis, the model is tested for disparate impact across groups, with impact measured and managed. The design and testing are documented, creating a defensible regulatory record, and fairness is monitored over time to detect drift. The model underwrites faster and more accurately within fair lending limits, because compliance, proxy avoidance, explainability, disparate-impact testing, shaped its design rather than being reviewed at the end.

Common Misconception

A more accurate underwriting model is a better one.

A more accurate model that discriminates by proxy, cannot be explained, or has untested disparate impact is a fair lending violation, not an advance, regardless of accuracy. In underwriting, a regulated decision, the model must be lawful and explainable, which is determined by design, not predictive performance.

Key Takeaway: Accuracy is not compliance. Whether mortgage AI is an advance or a violation depends on its features, explainability, and disparate-impact testing, not its predictive performance.

Real-World Compliant Mortgage AI in Action

Let's take a look at how compliant design operates with a real-world example.

We worked with a team building underwriting AI focused on accuracy, with these constraints:

- Avoid discrimination, directly and by proxy

- Make decisions explainable

- Test for disparate impact

Step 1: Vet the Features

Avoid proxies.

- Protected characteristics excluded

- Proxies avoided

- Features vetted for indirect discrimination

Step 2: Build Explainability

Meet legal requirements.

- Decisions explainable to applicants and regulators

- Adverse-action reasons producible

- Drivers transparent

Step 3: Test Disparate Impact

Measure fairness.

- Disparate impact tested across groups

- Impact measured and managed

- Risk identified before deployment

Step 4: Document the Design

Create a defensible record.

- Design and testing documented

- Feature legitimacy recorded

- Regulatory record maintained

Step 5: Govern Over Time

Maintain compliance.

- Fairness monitored

- Impact drift detected

- Ongoing governance

Where It Works Well

- Features avoiding protected characteristics and proxies

- Explainable decisions meeting legal requirements

- Disparate-impact testing and ongoing governance

Where It Does Not Work Well

- Optimizing accuracy with proxy features

- Opaque decisions that cannot be explained

- Untested disparate impact

Key Takeaway: The mortgage AI that is an advance rather than a violation is the one whose design, proxy avoidance, explainability, disparate-impact testing, meets fair lending, not the accurate model that cannot.

Common Pitfalls

i) Optimizing accuracy alone

An accurate model that discriminates by proxy or cannot be explained is a violation. Design for fair lending, not just accuracy.

- Avoid proxies

- Build explainability

- Test disparate impact

ii) Proxy features

Features correlated with protected characteristics cause indirect discrimination. Vet and avoid them.

iii) Unexplainable decisions

Applicants and regulators are entitled to explanations. An unexplainable model cannot meet fair lending. Build explainability.

iv) Untested disparate impact

Fair lending requires testing for disparate impact. An untested model carries unmanaged risk. Test before and after deployment.

Takeaway from these lessons: Most mortgage AI fair lending risk traces to proxies, opacity, and untested impact, not to accuracy. Avoid proxies, be explainable, and test disparate impact.

Compliant Mortgage AI Best Practices: What High-Performing Teams Do Differently

1. Design for fair lending, not just accuracy

Features, explainability, and disparate-impact testing determine compliance. Design them in from the start, not at the end.

2. Avoid proxies

Exclude protected characteristics and vet features for indirect discrimination through correlation. Proxy discrimination is still discrimination.

3. Build explainability

Make decisions explainable to applicants and regulators, with adverse-action reasons producible as the law requires.

4. Test disparate impact

Test for disparate impact across groups before and after deployment, measuring and managing it.

5. Document and govern

Document the design and testing for regulatory defensibility, and monitor fairness over time to detect drift.

Logiciel'svalue add is helping lending teams design underwriting AI that avoids proxies, is explainable, and is tested for disparate impact, so the model underwrites within fair lending limits rather than becoming a violation.

Takeaway for High-Performing Teams: Focus on the design that meets fair lending, proxy avoidance, explainability, disparate-impact testing, not just accuracy. In a regulated decision, mortgage AI is an advance when it is lawful and explainable, and a violation when it is not.

Signals You Are Underwriting Within Fair Lending Limits

How do you know the model is compliant? Not in its accuracy, but in its features, explainability, and testing. Below are the signals that distinguish a compliant model from a liability.

Features avoid proxies. The team excludes protected characteristics and vets features for indirect discrimination.

Decisions are explainable. The team can explain a decision to an applicant and a regulator and produce adverse-action reasons.

Disparate impact is tested. The team tests for disparate impact across groups and manages it.

The design is documented. The team has a defensible record of design and testing.

Fairness is monitored. The team monitors fairness over time and detects impact drift.

Adjacent Capabilities and Connected Work

This work does not exist in isolation. Compliant mortgage AI depends on, and feeds into, several adjacent capabilities. Building one without thinking about the others is the most common scoping mistake.

In most lending organizations, underwriting AI shares infrastructure with the loan origination and data systems, the model development process, and the compliance and legal function. It shares capacity with data science, product, and compliance. And it shares leadership attention with whatever the next lending-technology initiative is on the roadmap. Naming these adjacencies upfront helps the program scope realistically and helps leadership see the work as a portfolio rather than a one-off project.

The most common mistake in adjacent-capability scoping is treating each adjacency as someone else's problem. The features the model uses are your problem to vet. The explainability for adverse action is your problem. The disparate-impact testing is your problem. Pretending otherwise pushes work to teams that did not plan for it, and the work returns to you later as a fair lending violation. Own the adjacencies you depend on; partner with the teams that own them; share the timeline.

Conclusion

Mortgage AI within fair lending limits avoids proxy discrimination, is explainable to applicants and regulators, and is tested for disparate impact, compliance determined by design, not accuracy. The discipline that delivers it is the same discipline behind any regulated decision system: design for the legal requirements, test against them, and document the result.

Key Takeaways:

- Accuracy is not compliance; design determines fair lending risk

- Avoid protected characteristics and their proxies

- Build explainability, test disparate impact, and govern over time

Building compliant mortgage AI requires feature, explainability, and testing discipline. When done correctly, it produces:

- Underwriting that does not discriminate, directly or by proxy

- Explainable decisions meeting legal requirements

- Tested, managed disparate impact

- A documented, governed, defensible model

Silent Lead Leakage Is Killing Revenue Growth

Discover how 1–8% of real estate leads disappear before reaching your CRM.

What Logiciel Does Here

If you are building underwriting AI, design it for fair lending: avoid proxies, build explainability, test for disparate impact, and document the design before you deploy.

Learn More Here:

- AI Governance for Fair Housing: What Your Model Must Not Do

- Tenant Screening AI: Risk Models That Don't Violate Fair Housing

- Responsible AI and Compliance Frameworks

At Logiciel Solutions, we work with lending and technology leaders on fair-lending-compliant underwriting AI, explainability, and disparate-impact testing. Our reference patterns come from production lending models in regulated environments.

Explore how to automate mortgage underwriting within fair lending limits.

Frequently Asked Questions

What does fair lending require of an underwriting model?

That its decisions do not discriminate on protected characteristics, directly or indirectly through proxies; that decisions are explainable to applicants and regulators, including adverse-action reasons; and that the model is tested for disparate impact. These requirements shape the model's design, not just a final review.

What is proxy discrimination in mortgage AI?

Discrimination that occurs indirectly when a model uses features correlated with protected characteristics, even if the protected characteristics themselves are excluded. Avoiding proxy discrimination requires vetting features for indirect correlation, not just removing protected attributes.

Why must underwriting decisions be explainable?

Because applicants are legally entitled to explanations for adverse decisions and regulators expect them. An unexplainable model cannot produce the required adverse-action reasons or be defended, so explainability is a legal requirement, not a nice-to-have.

What is disparate-impact testing?

Testing whether a model's decisions have a disproportionate adverse effect on protected groups, even absent intent. Fair lending requires it; an untested model carries unknown, unmanaged risk. Testing should happen before deployment and on an ongoing basis.

What is the biggest mistake in mortgage underwriting AI?

Optimizing for predictive accuracy and confronting fair lending late, after proxy features, opaque decisions, and untested disparate impact are built in. A more accurate model that violates fair lending is a liability, not an advance. Design for proxy avoidance, explainability, and disparate-impact testing from the start.