Where AI Fits in Commercial Real Estate Underwriting

Commercial real estate underwriting has used quantitative models for decades. Discounted cash flow analysis. Cap rate analysis. Sensitivity testing. The work has been spreadsheet-heavy and analyst-driven. AI in 2026 has changed parts of this work without replacing the analyst judgment that drives final investment decisions.

The pattern is augmentation rather than replacement. AI handles data gathering, structured analysis, and scenario generation faster than analysts can. Analysts then apply judgment to the AI-enabled analysis. The combined throughput is significantly higher than the analyst-only baseline.

An investment director at a commercial real estate firm described their transition to me last year. "Our analysts used to spend 60% of their time gathering and structuring data. They now spend 20% on that and 60% on analysis and judgment. The throughput is up. The deals are getting better attention." The reflection captures what is happening across institutional commercial real estate.

The patterns for commercial real estate AI underwriting have settled enough through 2024 and 2025 to be reference material. The patterns differ from residential AI underwriting because the data sources, the decision stakes, and the workflow patterns are different.

Healthcare Data Standardization

Why clinical AI accuracy degrades when code sets update, how ontology mapping breaks across EHR vendors, and the canonical data layer.

Data Gathering and Structuring

Data gathering is the highest-volume AI use case in commercial real estate underwriting. The work involves pulling property data, market data, comparable transactions, tenant data, and various other inputs from many sources into a structured form analysts can use.

Property data comes from broker submissions, CoStar, Reis (now Moody's CRE), Real Capital Analytics, public records, and various other sources. The data has varying quality, varying granularity, and varying conventions. AI handles the normalization across sources.

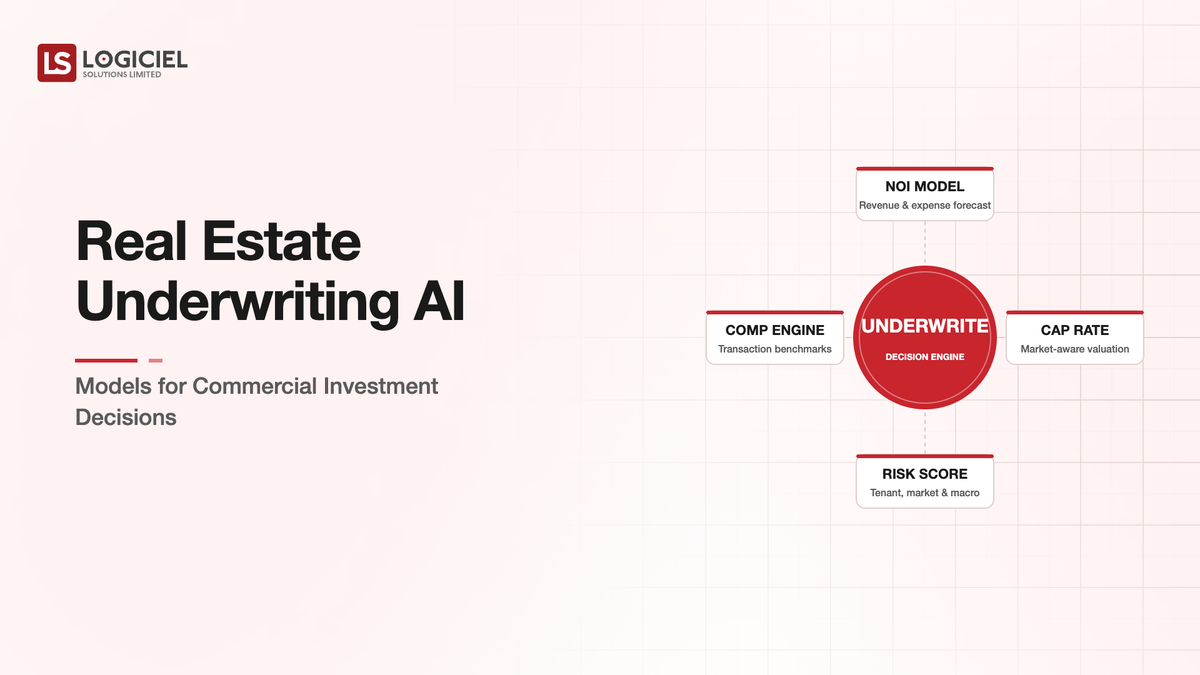

Comparable transaction data drives the valuation work. The AI identifies relevant comparables based on property type, location, size, age, tenant profile, and other characteristics. The identification is faster and more comprehensive than manual search.

Tenant data informs underwriting for tenant-driven asset classes (office, retail, industrial). The AI pulls public tenant information, financial data where available, and news indicators. The tenant credit assessment uses the data to inform underwriting assumptions.

Market data informs the broader context. Submarket rent trends. Vacancy rates. Construction pipeline. Economic indicators. The data assembles into a market context that the analyst can review and refine.

Document Processing and Lease Abstraction

Document processing has been one of the highest-ROI AI deployments in commercial real estate underwriting. The work involves extracting structured data from leases, financial statements, surveys, environmental reports, and various other documents that flow through the underwriting process.

Lease abstraction is the highest-value document use case. Commercial leases are long and complex. The terms that matter for underwriting include the basic financial structure, the escalation patterns, the expense recovery provisions, the renewal options, and the various conditional clauses. AI extracts this information into structured form for analyst review.

The accuracy has reached the level where the AI output can be used as a draft rather than a starting point. The analyst reviews the extracted data, focuses on the complex clauses, and corrects any errors. The time savings versus full manual abstraction is significant.

Financial statement processing pulls key financials from operating statements, rent rolls, and historical financials. The extraction handles the various formats that come from different property management systems and accounting practices.

Environmental and physical condition reports get processed for the issues that affect underwriting. Phase I and Phase II reports. Property condition assessments. The processing identifies the key findings without requiring the analyst to read the full reports for each property.

Title and zoning information processing handles the legal and regulatory context. The processing produces summaries that inform the legal due diligence work.

Scenario Generation and Stress Testing

Scenario generation has become an AI strength in commercial underwriting. The work involves generating plausible market and operational scenarios that the underwriting model is tested against.

Macro scenarios consider interest rate, inflation, and economic growth variations. The AI generates scenarios consistent with historical patterns and current economic context. The scenarios feed into the underwriting sensitivity analysis.

Market-specific scenarios consider submarket variations. Specific submarkets have different rent and occupancy trajectories. The AI generates scenarios consistent with the submarket history and current dynamics.

Property-specific scenarios consider operational variations. Tenant departure risk. Capital expenditure timing. Lease-up assumptions. The scenarios test the underwriting against operational variations that may affect returns.

Stress testing combines the scenarios with the underwriting model. The output shows how returns vary across the scenario space. The analyst identifies the scenarios that matter most and considers what they imply for the investment decision.

The pattern produces more comprehensive sensitivity analysis than manual scenario generation. The patterns are particularly useful for institutional underwriting where the sensitivity analysis is part of the documented investment decision.

The Limits of AI in Underwriting

Several aspects of commercial real estate underwriting remain analyst-driven. The limits are operationally important because they determine where AI investment pays off and where it does not.

Final investment judgment remains human. The decision to invest, to pass, or to negotiate is made by analysts and investment committees. AI informs the decision; it does not make the decision. The pattern reflects the stakes (commercial real estate investments are typically large and have long-term consequences) and the unstructured factors that influence the decision.

Relationship-driven information is hard for AI to capture. Conversations with brokers, owners, and tenants produce information that does not appear in documents or public data. The analyst's judgment about the seller's motivation, the tenant's intentions, and the broker's positioning shapes the underwriting in ways AI cannot replicate.

Unusual deal structures require analyst judgment. Standard transactions fit AI underwriting well. Unusual structures (complex joint ventures, programmatic deals, distressed situations) require judgment that AI does not provide.

Market intuition matters for deals that are at the edges of underwriting parameters. The analyst's read on whether a market is about to turn, whether a specific asset has hidden value, or whether a deal carries unappreciated risk shapes decisions in ways that quantitative analysis cannot fully capture.

Negotiation and structuring remain human work. The terms of a deal evolve through negotiation. AI can support the negotiation by analyzing alternative structures; it does not conduct the negotiation.

What Modern Commercial Real Estate AI Underwriting Looks Like

The reference patterns in 2026 share recognizable components across institutional commercial real estate investors that have integrated AI into underwriting.

Data gathering and structuring automation that produces underwriting-ready data from many sources. The automation handles the volume; analysts focus on judgment.

Document processing for leases, financials, and due diligence reports. The processing provides drafts that analysts review and refine.

Scenario generation and stress testing that produces more comprehensive sensitivity analysis than manual approaches. The patterns support documented investment decisions.

Integration with existing underwriting tools (Argus, Yardi Investment Management, internal models). The AI feeds into rather than replaces the existing tools.

Analyst workflow that uses AI for the work AI handles well and reserves analyst time for judgment work. The workflow is intentional rather than emergent.

Governance and audit trails for AI-influenced underwriting. The decisions and the underlying analyses are documented. The institutional investors that have integrated AI have done so with attention to the institutional governance requirements.

The patterns are not specific to any single asset class. Office, industrial, retail, multifamily, hotel, and other commercial asset classes all benefit from similar patterns adapted to the specific characteristics.

Ambient Clinical Documentation

The three engineering challenges that determine whether ambient AI documentation ships into a health system or fails security review.

What Logiciel Does Here

Logiciel works with commercial real estate investors and PropTech companies building AI underwriting capabilities. The work is typically structured around use case selection, data infrastructure design, and integration with existing underwriting tools alongside the AI development.

The AI Implementation framework covers the broader patterns. The Data Engineering for Real Estate framework covers the data integration work that underwriting AI requires.

A 30-minute working session is enough to assess your underwriting AI strategy against the 2026 patterns.

Frequently Asked Questions

Should we build our own underwriting AI or use vendor tools?

Most institutional investors use a combination. Vendor tools handle data gathering, document processing, and standard analytics. Internal development focuses on proprietary underwriting models and the integration with the firm's specific workflow. Building everything is expensive and rarely produces commensurate differentiation.

What is the impact on analyst headcount?

Varies by firm strategy. Some firms have kept similar headcount and raised the deal count or the depth per deal. Some firms have reduced headcount in roles where AI handles the work. The pattern depends on the firm's growth ambitions and operational structure.

How accurate is AI lease abstraction?

Reaching levels where analysts can use the AI output as a draft rather than a starting point. Specific accuracy varies by lease type, language, and the specific AI tools used. The 2026 vendor offerings (Lease Sense, Prophia, Leverton, custom implementations) have all advanced significantly through 2024.

What about AI for residential underwriting (mortgages)?

Different domain with different regulatory considerations. Residential mortgage AI faces fair lending constraints that commercial does not. The patterns and the regulatory environment are different enough that residential and commercial AI underwriting should be treated as separate disciplines.

How do investment committees treat AI-supported underwriting?

Increasingly comfortable when the AI involvement is documented. Investment committees want to understand what AI did versus what analysts did. They want assurance that the AI work was reviewed. The patterns are similar to other quantitative methods that committees have evaluated over the years. ## Sources: NAIOP Commercial Real Estate Research, 2024 ULI Commercial Real Estate Trends, 2024 CCIM Institute Commercial Real Estate Reports, 2024